Disclosures and Terms & Conditions for Your Business Account

Updated June 2025

{beginAccordion}

Terms & Conditions

Important Information About Procedures for Opening a New Account

Agreement

Copy of this Agreement

Limitation Period For Bringing Legal Action

Costs and Attorneys’ Fees/Indemnification/Limitation of Liability/Waiver of Claims

Arbitration Provision

Liability

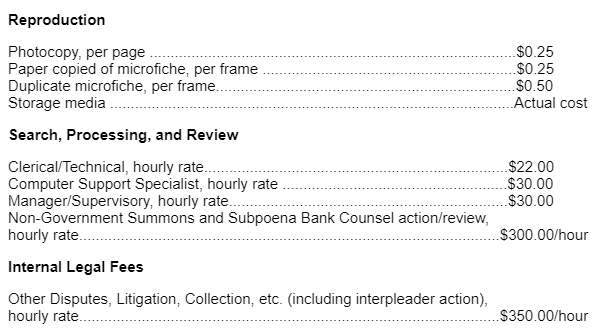

Summons and Subpoena Cost Reimbursement Schedule

Deposits

Items Returned

Withdrawals

Dormant Account

Understanding and Avoiding Overdraft and Nonsufficient Funds (NSF) Fees

Business, Organization and Association Accounts

Stop Payments

ACH Stop Payments

Telephone Transfers

Amendments and Termination

Correction of Clerial Errors

Notices

Statements

Account Transfer

Reimbursement of Federal Benefit Payments

Temporary Account Agreement

Setoff

Restrictive Legends or Indorsements

Facsimile/Electronic Signatures

Check Processing

Automated Processing of Items

Check Cashing

Indorsements

Stale-Dated Checks

Death or Incompetence

Fiduciary Accounts

Credit Verification

Legal Actions Affecting Your Account

Reporting Negative Information to Credit Bureaus; Disputing Reporting Information

Account Security

Positive Pay and Other Fraud Prevention Services

Instructions From You

Monitoring and Recording Telephone Calls and Account Communications

Claim of Loss

Early Withdrawal Penalties

Changes in Name and Contact Information

Resolving Account Disputes

Waiver of Notices

Funds Transfer

International ACH Transactions

Truncation, Substitute Checks, and Other Check Images

Remotely Created Checks

Unlawful Internet Gambling Notice

Funds Transfers

Subaccount Organization

Important Information About Procedures for Opening a New Account To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account.

What this means for you: When you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver's license or other identifying documents.

AGREEMENT - This Agreement ("agreement" or "Agreement"), along with any other documents we give you pertaining to your account(s), is a contract (also referred to as "this agreement") that establishes rules which control your account(s) with us. Please read this carefully and retain it for future reference. If you open the account (whether in-person, electronically, or by any other method permitted by us) or open or continue to use the account after receiving a notice of change or amendment, you agree to these rules. You will receive a separate schedule of rates, qualifying balances, and fees if they are not included in this agreement. If you have any questions, please ask us.

This agreement is subject to applicable federal laws, including the Federal Arbitration Act, the laws of the state of Colorado and other applicable rules such as the operating letters of the Federal Reserve Banks and payment processing system rules (except to the extent that this agreement can and does vary such rules or laws). The body of state and federal law that governs our relationship with you, however, is too large and complex to be reproduced here. The purpose of this agreement is to:

- summarize some laws that apply to common transactions;

- establish rules to cover transactions or events which the law does not regulate;

- establish rules for certain transactions or events which the law regulates but permits variation by agreement; and

- give you disclosures of some of our policies to which you may be entitled or in which you may be interested.

If any provision of this agreement is found to be unenforceable according to its terms, all remaining provisions will continue in full force and effect. We may permit some variations from our standard agreement, but we must agree to any variation in writing either on the signature card for your account or in some other document. Nothing in this agreement is intended to vary our duty to act in good faith and with ordinary care when required by law.

As used in this agreement the words "we," "our,” “Us,” “The Bank,” and "Alpine Bank" mean the financial institution and the words "you" and "your" mean the account holder(s) and anyone else with the authority to deposit, withdraw, or exercise control over the funds in the account. The headings in this agreement are for convenience or reference only and will not govern the interpretation of the provisions. Unless it would be inconsistent to do so, words and phrases used in this agreement should be construed so the singular includes the plural and the plural includes the singular.

COPY OF THIS AGREEMENT - You acknowledge and agree that we may destroy this original account Agreement once the Agreement has been electronically archived. A copy of this Agreement maintained in our record-keeping system may be used for any purpose and shall be legally binding to the same extent as the original.

LIMITATION PERIOD FOR BRINGING LEGAL ACTION - An action or proceeding by you to enforce an obligation, duty or right arising under this Agreement or by law with respect to your account(s) or any account service(s) must be commenced within one (1) year after the cause of action accrues.

COSTS AND ATTORNEYS' FEES/INDEMNIFICATION/LIMITATION OF LIABILITY/WAIVER OF CLAIMS - You agree to reimburse us for any and all claims, damages, losses, liabilities, expenses and, to the extent permitted by law, costs including reasonable attorneys’ fees and collection agencies’ fees, we incur with respect to the collection of overdrafts or other amounts due from you under this Agreement, or otherwise in connection with your account. We will not be responsible for any loss to you caused by an event that is beyond our control, including, but not limited to, natural disasters, pandemics or epidemics, wars, acts of terrorists, riots, strikes, computer failure, or the loss or interruption of power, communication, or transportation facilities. We will not be responsible for any acts or omissions of a third party not under our direct control, including without limitation, a clearinghouse, service provider, or Federal Reserve Bank. In no event shall we be liable to you for special, punitive, or consequential damages from the performance of services in connection with the account, unless otherwise required by law. There are no third party beneficiaries of this Agreement and we will not be responsible to any third party for services performed in connection with this Agreement. WAIVER OF CLAIMS: YOUR FAILURE TO REPORT ANY ACCOUNT DISPUTE OR DIFFERENCE, ERROR, UNAUTHORIZED TRANSACTION, FEE OR OTHER CHARGE ASSESSED TO YOUR ACCOUNT(S) UTILIZING THE ERROR RESOLUTION GUIDELINES AND THE NOTICE DEADLINES SET FORTH IN SECTION STATEMENTS OF THIS AGREEMENT, OR IN SECTION FUNDS TRANSFERS-DUTY TO REPORT UNAUTHORIZED OR ERRONEOUS PAYMENT OF THIS AGREEMENT FOR AN EFT TRANSACTION OR SERVICE, SHALL PRECLUDE YOU FROM RECOVERING ANY AMOUNTS FROM US AND YOU HEREBY WAIVE ALL LEGAL CLAIMS RELATED TO ANY SUCH FEES OR SERVICES ASSOCIATED WITH YOUR ACCOUNT THAT WERE REFLECTED ON YOUR STATEMENT, OR THAT ARE ON OUR FEE SCHEDULE. YOU ACKNOWLEDGE THAT THIS IS A MATERIAL TERM TO THE CONTRACT BETWEEN YOU AND US. YOU FURTHER ACKNOWLEDGE THAT IF YOU ARE NOT SATISFIED WITH A FEE OR SERVICE THAT YOU MAY CHANGE BANKS AT ANY TIME. IF YOU HAVE A SEPARATE CONTRACT WITH US ASIDE FROM THIS AGREEMENT, THAT CONTRACT WILL CONTROL AS TO ANY APPLICABLE NOTICE PROVISIONS.

This arbitration provision is optional. If you do not wish to accept it, you must follow the instructions in paragraph 11 below to reject arbitration. Unless you timely reject arbitration, this arbitration provision is binding on you and us.

(1) Claims Subject to Arbitration: Except as specified in paragraph (2) below, any dispute or claim between you and us must be arbitrated if either party elects arbitration of that dispute or claim. This agreement to arbitrate is intended to be broadly interpreted. It includes, but is not limited to:

• claims arising out of or relating to any aspect of the relationship between you and us, whether based in contract, tort, fraud, misrepresentation, or any other statutory or common-law legal theory;

• claims that arose before this or any prior agreement (including, but not limited to, claims relating to advertising or disclosures for any of our products or services);

• claims for mental or emotional distress or injury not arising out of bodily injury;

• claims asserted in a court of general jurisdiction against you or us, including counterclaims, cross-claims, or third-party claims, that you or we elect to arbitrate in the answer or other responsive pleading;

• claims relating to the retention, protection, use, or transfer of information about you or any of your accounts for any of our products or services;

• claims relating to communications with you, regardless of sender, concerning any of our products or services, including emails and automatically dialed calls and text messages; and

• claims that may arise after the termination of this Agreement.

In this arbitration provision only, references to "we" and "us" mean the financial institution and its past, present, and future parents, subsidiaries, affiliates, and each of these entities’ predecessors, successors, assigns, agents, and employees. In this arbitration provision only, references to "you" mean the account owners, all authorized or unauthorized users or beneficiaries of the account, each of those person's assignees, heirs, trustees, agents, or other representatives, and if the account owner is a business, the account owner's parents, subsidiaries, affiliates, and each of those entities' predecessors, successors, assigns, agents, and employees. This arbitration agreement does not preclude you or us from bringing issues to the attention of federal, state, or local agencies. Such agencies can, if the law allows, seek relief against you or us on the other's behalf. Nor does this arbitration agreement preclude either you or us from exercising self-help remedies (including setoff) and exercising such a remedy is not a waiver of the right to invoke arbitration of any dispute. You and we each waive the right to a trial by jury or to participate in a class action whenever either you or we elect arbitration. This agreement evidences a transaction in interstate commerce, and thus the Federal Arbitration Act governs the interpretation and enforcement of this provision. This arbitration provision shall survive termination of this agreement.

(2) Claims Not Subject to Arbitration: You and we agree that the following disputes or claims cannot be arbitrated:

• claims arising from bodily injury or death;

• claims seeking only individualized relief asserted by you or us in small claims court, so long as the action remains in that court and is not removed or appealed de novo to a court of general jurisdiction;

• claims to collect or challenge debts owed pursuant to an extension of credit under a separate agreement or note (such as a separate loan agreement, promissory note, or bank card agreement), in which case the dispute over the debt shall be governed by the dispute-resolution procedures set forth in that separate agreement or note;

• disputes over the scope and enforceability of this arbitration provision, whether a dispute or claim can or must be brought in arbitration, or whether paragraphs (7) or (8) of this arbitration provision have been violated; and

• disputes over whether paragraph (4) has been violated, unless the parties have agreed to submit the dispute to a process arbitrator.

(3) Pre-Arbitration Notice of Disputes and Informal Resolution: Before either you or we commence arbitration, the claimant must first send to the other a written Notice of Dispute ("Notice"). The Notice to us should be sent by U.S. mail or professional courier service to:Alpine Bank Attn: Collection Department, 400 7th Street South Rifle, CO 81650 ("Notice Address"). The Notice to you will be sent to your address on file with your account. The Notice must (a) include your name, phone number, mailing and email address; (b) the account number for any account at issue; (c) describe the nature and basis of the claim or dispute; and (d) set forth the specific relief sought. The Notice must be personally signed by you (if you are the claimant) or by our representative (if we are the claimant). To safeguard your account, if you have retained a lawyer to submit your Notice, you must also provide with the Notice your personally signed written authorization allowing us to discuss the Notice, the dispute, and your account(s) with your lawyer (“Attorney Authorization”). We may also ask you to verify your identity and the fact that you authorized submission of the Notice or disclosure of account information to your lawyer (“Verification”). You agree to cooperate with any reasonable request for Verification.

Whoever sends the Notice must give the other party 60 days after receipt of a complete Notice (including an Attorney Authorization if you are represented by a lawyer and a Verification if requested) to investigate the claim. During that period, either you or we may request an individualized discussion (by phone call or videoconference) regarding settlement (“Informal Settlement Conference”). You and we must work together in good faith to select a mutually agreeable time for the Informal Settlement Conference (which can be after the 60-day period). You and our representative must both personally participate, unless otherwise agreed in writing. Your and our lawyers (if any) also can participate.

Any applicable statute of limitations or contractual limitations period will be tolled during the “Informal Resolution Period.” The Informal Resolution Period is the number of days between the date that a complete Notice (including an Attorney Authorization if you are represented by a lawyer and a Verification if requested) is received by the other party and the later of (i) 60 days later or (ii) the date the Informal Settlement Conference is completed, if timely requested.

(4) Commencing Arbitration: An arbitration proceeding cannot be commenced until after the Informal Resolution Period has ended and the pre-arbitration requirements in paragraph (3) have been satisfied. (Paragraph (8) has additional requirements for commencing certain coordinated arbitrations.) A court will have authority to enforce this paragraph (4), including the power to enjoin the filing or prosecution of arbitrations without first providing a complete Notice and participating in a timely requested Informal Settlement Conference. The court also may enjoin the assessment or collection of arbitration fees incurred as a result of such arbitrations. Further, unless prohibited by applicable law, the arbitration provider shall not accept nor administer any arbitration nor assess any fees in connection with an arbitration unless the claimant has complied with the Notice and Informal Settlement Conference requirements of paragraph (3). If a process arbitrator has been appointed at the request of a party, the process arbitrator also has the same authority as a court to enforce this paragraph (4).

(5) Arbitration Procedure: The arbitration will be governed by the Consumer Arbitration Rules and, if applicable, the Mass Arbitration Supplementary Rules ("AAA Rules") of the American Arbitration Association ("AAA"), as modified by this arbitration provision, and will be administered by the AAA. (If the AAA is unavailable or unwilling to administer arbitrations consistent with this arbitration provision, another arbitration provider shall be selected by the parties or by the court.) The AAA Rules are available online at www.adr.org or by writing to the Notice Address

Unless you and we agree otherwise, any arbitration hearings will take place in the county of your address on file with your account. If appropriate, the arbitrator may hold hearings by telephone or videoconference or decide matters on the basis of papers submitted by the parties. Regardless of the manner in which the arbitration is conducted, the arbitrator shall issue a reasoned written decision sufficient to explain the essential findings and conclusions on which the award is based.

Except as provided in paragraph (7) below, the arbitrator shall apply the same substantive law that a court would apply and can award the same individualized remedies (including punitive and statutory damages and statutory attorney's fees and costs) that a court could award under applicable law. The arbitrator may consider rulings in arbitrations involving different customers, but an arbitrator’s ruling will not be binding in proceedings involving different customers. As in court, you and we agree that any counsel representing someone in arbitration certifies that they are complying with the requirements of Federal Rule of Civil Procedure 11(b), and the arbitrator is authorized to impose any sanctions available under that rule, the AAA Rules, or applicable federal or state law against all appropriate represented parties or counsel.

During the arbitration, the amount of any settlement offer shall not be disclosed to the arbitrator until after the arbitrator determines the amount, if any, to which you are entitled. If you have complied with the requirements of this paragraph and paragraph (3) and the arbitrator awards you an amount of money that exceeds the value of our last written settlement to you before the appointment of the arbitrator, then we will pay you $1,000 in lieu of any smaller award. In determining whether you are entitled to the minimum $1,000 recovery, the arbitrator shall not consider amounts offered or awarded for attorneys' fees or costs. Any disputes as to payment of the $1,000 minimum recovery shall be resolved by the arbitrator, and must be raised within 14 days of the arbitrator's ruling on the merits.

(6) Arbitration Fees: We will pay all AAA filing, administration, case-management, hearing, and arbitrator fees (“AAA Fees”) if we initiate an arbitration. Except as specified below, if you initiate arbitration of claims seeking relief valued at $10,000.00 or less, we will pay the AAA Fees, so long as you have fully complied with the requirements in paragraphs (3) and (4). In such cases, we will pay the filing fee directly to AAA upon receiving a written request from you at the Notice Address or, if AAA requires you to pay the filing fee to commence arbitration, we will send that amount to the AAA and request that the AAA reimburse you. If, however, the arbitrator finds that you or your counsel have violated the standards of Federal Rule of Civil Procedure 11(b), then the payment and allocation of AAA Fees will be governed by the AAA Rules, and you may be required to reimburse us for AAA Fees that we paid on your behalf. In addition, if you initiate an arbitration in which you seek relief valued at greater than $10,000 (either to you or to us), the payment of AAA Fees will be governed by the AAA rules. Moreover, regardless of the value of the relief sought in an arbitration, if the AAA’s Mass Arbitration Supplementary Rules and fee schedule apply to your arbitration, the parties will each be responsible for paying their share of any fees assessed by the AAA under those rules and fee schedule. In any case, if you cannot afford your share of such fees, you may request a fee waiver from the AAA. If the AAA declines to waive the fees (after submission of any required documentation), we will consider any reasonable written request to reimburse your share of the fees or pay them directly.

(7) Requirement of Individual Arbitration: The arbitrator may award relief (including damages, restitution, and declaratory or injunctive relief) only in favor of the individual party seeking relief and only to the extent necessary to provide relief warranted by that party's individual claim. YOU AND WE AGREE THAT EACH MAY BRING CLAIMS AGAINST THE OTHER ONLY IN YOUR OR OUR INDIVIDUAL CAPACITY, AND NOT AS A PLAINTIFF OR CLASS MEMBER IN ANY PURPORTED CLASS, REPRESENTATIVE, OR PRIVATE ATTORNEY GENERAL PROCEEDING. Further, unless both you and we agree otherwise, the arbitrator may not consolidate the claims of more than one person (except for the claims of co- or joint account owners pertaining to that account), and may not otherwise preside over any form of a representative, class, or private attorney general proceeding. If, after exhaustion of all appeals, any of these prohibitions on non-individualized relief and proceedings or on consolidation are found to be unenforceable, then all other aspects of the case must be arbitrated first. After completing arbitration, the remaining (non-arbitrable) aspects of the case will then be decided by a court.

(8) Coordinated Arbitrations: If 25 or more claimants submit Notices or seek to file arbitrations raising similar claims and are represented by the same or coordinated counsel (whether the cases are pursued simultaneously or not), all the cases must be resolved in staged proceedings. You agree to this process even though it may delay the arbitration of your claim. In the first stage, we and claimants’ counsel will each select up to 25 cases (50 cases total) to be filed in arbitration and resolved individually by different arbitrators. In the meantime, no other cases may be filed or proceed in arbitration, and the arbitration administrator must not assess or demand payment of fees for the remaining cases or administer or accept them.

The arbitrators are encouraged to resolve the cases within 120 days of appointment or as swiftly as possible thereafter, consistent with fairness to the parties. After the first stage is completed, the parties must engage in a single mediation of all remaining cases, with us paying the mediation fee. If the parties cannot agree how to resolve the remaining cases after mediation, they will repeat the process of selecting and filing up to 50 cases to be resolved individually by different arbitrators, followed by mediation.

If any claims remain after the second stage, the process will be repeated until all claims are resolved, with four differences. First, a total of 100 cases may be filed in the third and later stages. Second, the cases will be randomly selected. Third, arbitrators who decided cases in the first two stages may be appointed in later stages if different arbitrators are not available. Fourth, mediation is optional at the election of claimants’ counsel.

Between stages, counsel will meet and confer regarding ways to improve the efficiency of the staged proceedings, including whether to increase the number of cases filed in each stage. Either party may also negotiate with the arbitration administrator regarding the amount or timing of arbitration fees.

If this paragraph applies to a Notice, the Informal Resolution Period for the claims and relief set forth in that Notice will be extended (including the tolling of any limitations periods) until that Notice is selected for a staged proceeding, withdrawn, or otherwise resolved. A court will have the authority to enforce this paragraph, including by enjoining the mass filing, the prosecution or administration of arbitrations, or the assessment or collection of arbitration fees.

This paragraph is intended to be severable from the rest of this arbitration provision. If, after exhaustion of all appeals, a court decides that the staging process is not enforceable, then the cases may be filed in arbitration and the payment of arbitration fees will be assessed as the arbitrations advance and arbitrators are appointed rather than when the arbitrations are initiated.

(9) Additional Procedures for Complex Disputes: If you are a business customer and the actual damages sought by either you or us in an arbitration exceeds $75,000 (not counting amounts sought for punitive, statutory, treble, or emotional harm damages or for attorneys’ fees or costs), then the AAA’s Commercial Arbitration Rules and fee schedule rather than the Consumer Arbitration Rules and consumer fee schedule shall apply. Regardless of whether you are a business or consumer customer, if the actual damages sought by either you or us in an arbitration exceeds $1,000,000 (not counting amounts sought for punitive, statutory, treble, or emotional harm damages or for attorneys’ fees or costs), then either party may appeal the final award to a three-arbitrator panel pursuant to the AAA’s Optional Appellate Rules by providing written notice within 30 days of the award. The appellant shall pay all fees and costs for the appeal unless the panel determines that the appellant is the prevailing party, in which case the panel shall have the discretion in its final award to reallocate the fees and costs as justice or otherwise applicable law requires. If there is a cross-appeal, the costs shall be borne equally by both sides, subject to reallocation by the panel in its final award as justice or otherwise applicable law requires.

(10) Future Changes to Arbitration Provision: Notwithstanding any provision in this Agreement to the contrary, you and we agree that if we make any future change to this arbitration provision (other than a change to the Notice Address), you may reject that change by sending us written notice within 30 days of notice of the change to the Notice Address. By rejecting that future change, you are agreeing that you will arbitrate any dispute or claim between you and us in accordance with the language of this provision, as amended by any changes that you did not timely reject.

(11) Right to Reject Arbitration Provision: If you do not wish to arbitrate, you have 30 days to reject this arbitration provision by sending a rejection notice to the Notice Address specified above in paragraph (3) ("Rejection Notice"). To be valid, a Rejection Notice must: (a) include your name, address, phone number, account number, and a statement that you are rejecting the arbitration provision in this agreement; and (b) be received by us within 30 days after the opening of your account. If an arbitration provision has been added for the first time to the agreement for an existing account, your Rejection Notice must be postmarked on or before the effective date of that amendment to that agreement. If your Rejection Notice complies with these requirements, this arbitration provision will not apply to you with respect to any claims that you or we commence in litigation or arbitration after we receive your Rejection Notice. Rejecting this arbitration provision will not affect your other rights or responsibilities under this agreement. Nor will it affect any other arbitration agreements between you and us, such as arbitration provisions in other contracts between you and us

(12) Military Lending Act: If you are a covered member of the armed forces or the dependent of a covered member within the meaning of the Military Lending Act and your Agreement with us involves an extension of consumer credit under that Act, then you are not required to arbitrate disputes.

FORUM SELECTION - Unless you and we agree otherwise, to the greatest extent permitted by law, the state and federal courts in or for Garfield County, Colorado, will have exclusive jurisdiction over any disputes (except for disputes brought in small claims court) that are not subject to arbitration or over any action involving the applicability or enforceability of the Arbitration Provision. You and we consent to the jurisdiction of those courts and waive any objections as to personal jurisdiction or venue in those courts or any right to seek to transfer or change venue of any such action to another court.

LIABILITY - You agree, for yourself (and the person or entity you represent if you sign as a representative of another) to the terms of this account and the schedule of charges. You authorize us to deduct these charges, without notice to you, directly from the account balance as accrued. You will pay any additional reasonable charges for services you request which are not covered by this Agreement.

Each of you also agrees to be jointly and severally (individually) liable for any account shortage resulting from charges or overdrafts, whether caused by you or another with access to this account, or fraud, theft or embezzlement by a third party. This liability is due immediately, and we can deduct any amounts deposited into the account and apply those amounts to the shortage costs and fees (including attorneys’ fees). You have no right to defer payment of this liability, and you are liable regardless of whether you signed the item or benefited from the charge or overdraft. In the event we file suit to collect account shortages or overdrafts, you will be liable for all costs and reasonable attorney's fees incurred (both internal and external) regardless of whether the suit is withdrawn, dismissed (with or without prejudice), settled or stayed due to a bankruptcy filing.

You will also be liable for all costs and reasonable attorneys' fees (both internal and external), to the extent permitted by law, whether incurred as a result of collection effort, subpoena, summons, garnishment, levy, warrant, court order, investigation (including any internal investigation), research efforts, review of documents and communications or any type of dispute involving your account. This includes, but is not limited to, disputes between you and another joint owner; you and an authorized signer or similar party; or a third party claiming an interest in your account. This also includes any action that you or a third party takes regarding the account that causes us, in good faith, to seek the advice of an attorney (both internal and external), whether or not we become involved in the dispute. You will also be liable for all costs and reasonable attorneys' fees (both internal and external) incurred as a result of an interpleader action which we may initiate in our sole and absolute discretion. All costs and attorneys' fees can be deducted from your account when they are incurred, without notice to you.

If you provide account information that facilitates creation of a check that is presented to us without signature, you are liable for payment of the check. Thus if you voluntarily give information about your account (such as our routing number and your account number) to a party who is seeking to sell you goods or services, and you don’t physically deliver a check to the party, any debit to your account initiated by the party to whom you gave the information is deemed authorized. You agree to indemnify us from any claim against or loss incurred by us as a result of any demand draft or remotely created check drawn on or deposited into your account. This indemnity includes reasonable attorney fees incurred by us.

Summons and Subpoena Cost Reimbursement Schedule -

DEPOSITS - It's your responsibility, not ours, to confirm the accuracy of the amount you deposit. You must notify us in a reasonable amount of time for any deposit discrepancies you may notice. If we determine a discrepancy exists between the declared and the actual amount, we may debit or credit your account accordingly. Any corrected deposit amounts will be reflected on your monthly account statement, and we may, at our discretion, notify you via USPS mail with the most recent address on our deposit records of adjustments made if the amount adjusted is over our standard adjustment notification amount.

We will give only provisional credit until collection is final for any items, other than cash, we accept for deposit (including items drawn "on us"). Before settlement of any item becomes final, we act only as your agent, regardless of the form of indorsement or lack of indorsement on the item and even though we provide you provisional credit for the item. We may reverse any provisional credit for items that are lost, stolen, or returned. Unless prohibited by law, we also reserve the right to charge back to your account the amount of any item deposited to your account or cashed for you which was initially paid by the payor bank and which is later returned to us due to an allegedly forged, unauthorized or missing indorsement, claim of alteration, encoding error, counterfeit cashier's check or other problem which in our judgment justifies reversal of credit. You authorize us to attempt to collect previously returned items without giving you notice, and in attempting to collect we may permit the payor bank to hold an item beyond the midnight deadline. Actual credit for deposits of, or payable in, foreign currency will be at the exchange rate in effect on final collection in U.S. dollars. We are not responsible for transactions by mail or outside depository until we actually record them. We will treat and record all transactions received after our "daily cutoff time" on a business day we are open, or received on a day we are not open for business, as if initiated on the next business day that we are open. At our option, we may take an item for collection rather than for deposit. If we accept a third-party check or draft for deposit, we may require any third-party indorsers to verify or guarantee their indorsements, or indorse in our presence.

ITEMS RETURNED -If a deposited item is returned to us by the bank on which it was drawn, we may accept that return and charge the item back against your account without regard to whether the other bank returned the item before its midnight deadline or otherwise finally paid the item. At our option and without prior notice to you, we have the right to pursue collection of previously dishonored items, including permitting a paying bank to hold an item beyond its midnight deadline in an attempt to recover payment. You waive presentment, notice of dishonor and protest, and agree that we have no obligation to notify you of any deposited item that is returned to us. Without prior notice to you, we may charge back any item at any time before final payment, whether returned or not. We may process a copy or other evidence of the returned item in lieu of the original. If an item deposited to your account or cashed for you has been paid by the paying bank and that bank later returns the item to us due to an allegedly forged, unauthorized or missing endorsement, claim of alteration, encoding error or other problem which in its judgment justifies reversal of credit, we reserve the right to charge back the item to your account.

If a deposited or cashed item is returned we can deduct the amount of the deposited or cashed item from your account even if you have withdrawn the funds and the balance in your account is not sufficient to cover the amount we hold or deduct. This could result in your account being overdrawn, and non-sufficient funds fees may be assessed.

We will determine your current available balance for overdraft purposes during our nightly processing following our cutoff time for transaction posting. At this time, items may be returned which have posted earlier in the day.

Important terms for accounts where more than one person can withdraw - Unless clearly indicated otherwise on the account records, any of you, acting alone, who signs to open the account or has authority to make withdrawals may withdraw or transfer all or any part of the account available balance at any time. Each of you (until we receive written notice to the contrary) authorizes each other person who signs or has authority to make withdrawals to indorse any item payable to you or your order for deposit to this account or any other transaction with us.

Postdated checks - A postdated check is one which bears a date later than the date on which the check is written. We may properly pay and charge your account for a postdated check even though payment was made before the date of the check, unless we have received written notice of the postdating in time to have a reasonable opportunity to act. Because we process checks mechanically, your notice will not be effective and we will not be liable for failing to honor your notice unless it precisely identifies the check number, date, amount and payee of the item.

Checks and withdrawal rules - We may refuse any withdrawal or transfer request which you attempt on forms not approved by us or by any method we do not specifically permit. We may refuse any withdrawal or transfer request which is greater in number than the frequency permitted by our policy, or which is for an amount greater or less than any withdrawal limitations. We will use the date the transaction is completed by us (as opposed to the date you initiate it) to apply any frequency limitations. In addition, we may place limitations on the account until your identity is verified.

Even if we honor a nonconforming request, we are not required to do so later. If you violate the stated transaction limitations (if any), in our discretion we may close your account or reclassify your account as another type of account. If we reclassify your account, your account will be subject to the fees and earnings rules of the new account classification.

If we are presented with an item drawn against your account that would be a "substitute check," as defined by law, but for an error or defect in the item introduced in the substitute check creation process, you agree that we may pay such item.

See the funds availability policy, the section titled Your Ability to Withdraw Funds, for information about when you can withdraw funds you deposit. For those accounts to which our funds availability policy disclosure does not apply, you can ask us when you make a deposit when those funds will be available for withdrawal. An item may be returned after the funds from the deposit of that item are made available for withdrawal. In that case, we will reverse the credit of the item. We may determine the amount of available funds in your account for the purpose of deciding whether to return an item for insufficient funds at any time between the time we receive the item and when we return the item or send a notice in lieu of return. We need only make one determination, but if we choose to make a subsequent determination, the account balance at the subsequent time will determine whether there are insufficient available funds.

Cash withdrawals - We recommend you take care when making large cash withdrawals because carrying large amounts of cash may pose a danger to your personal safety. As an alternative to making a large cash withdrawal, you may want to consider a cashier's check or similar instrument. You assume full responsibility of any loss in the event the cash you withdraw is lost, stolen, or destroyed. You agree to hold us harmless from any loss you incur as a result of your decision to withdraw funds in the form of cash.

Multiple signatures, electronic check conversion, and similar transactions - An electronic check conversion transaction is a transaction where a check or similar item is converted into an electronic fund transfer as defined in the Electronic Fund Transfers regulation. In these types of transactions the check or similar item is either removed from circulation (truncated) or given back to you. As a result, we have no opportunity to review the signatures or otherwise examine the original check or item. You agree that, as to these or any items as to which we have no opportunity to examine the signatures, you waive any requirement of multiple signatures. Please note that a merchant may attempt to collect on a converted check transaction up to three times.

Notice of withdrawal - We reserve the right to require not less than 7 days' notice in writing before each withdrawal from an interest-bearing account, other than a time deposit. Withdrawals from a time account prior to maturity or prior to any notice period may be restricted and may be subject to penalty. See your separately provided notice of penalty for early withdrawal titled “Early Withdrawal Penalties” within this document.

DORMANT ACCOUNT - Checking accounts with no deposit, withdrawal, or transfer transactions for 12 consecutive months, and savings accounts with no deposit, withdrawal, or transfer transactions for 24 consecutive months are considered dormant. To reactivate a dormant account you may: (a) make a deposit to or a withdrawal from the account; (b) update your signature card; or (c) provide a dated, signed and notarized correspondence specifically requesting the account be reactivated. We will try to contact you at the current address we have on file before we classify any account as dormant.

We reserve the right to not send statements to addresses that we have been notified by the United States Postal Service are insufficient.

Subject to applicable law, accounts may be charged dormant account fees in addition to the normal service charges (e.g., monthly service fees, paper statement fees, etc.) while the account is in dormant status, and we have an insufficient address. Please refer to your account Truth-in-Savings disclosure for the applicable monthly maintenance fees and the Fee Schedule for the current dormant account fee.

All interest-bearing accounts will continue to earn interest, even while in a dormant status. We may refuse to pay items drawn on or payable out of a dormant account. We may refuse a withdrawal or transfer from a dormant account if we cannot reach you in a timely manner to confirm the transaction.

We may be required to turn over (escheat) account funds to the state if you fail to do one of the following within the time period specified by Colorado State law, which is five (5) years: (a) make a deposit to or a withdrawal from the account; (b) update your signature card; or (c) provide a dated, signed and notarized correspondence specifically requesting the account be reactivated. It is important to understand that the correspondence provided will be applicable for the subsequent 12 months for a deposit account, or in the case of a savings account, 24 months.

We may impose a fee for sending an account escheat notice to you prior to turning the funds over to the state.

If funds are remitted to the state, you may file a claim with the state to recover the funds. For more information regarding Colorado Unclaimed Property law, please visit the Colorado State Treasurer's website at colorado.findyourunclaimedproperty.com.

UNDERSTANDING AND AVOIDING OVERDRAFT AND NONSUFFICIENT FUNDS (NSF) FEES -

Generally - The information in this section is being provided to help you understand what happens if your account is overdrawn. Understanding the concepts of overdrafts and non-sufficient funds (NSF) is important and can help you avoid being assessed fees or charges.

An overdrawn account will often result in you being charged an overdraft fee if we pay the item that overdraws the account. Generally, with some exceptions, an overdraft occurs when there is not enough money in your account’s available balance (see below) at the time we authorized and in your current balance at the time we pay for a transaction, but we pay (or cover) the transaction anyway. When we pay the transaction in your account, this is known as a Non-sufficient paid item or ‘NSF paid item fee’. An NSF transaction is slightly different. In an NSF transaction, we do not cover the transaction. Instead, the item or requested payment is returned. In this situation we refer to this as a Non-sufficient returned item. Importantly, we do not assess a fee if we return a transaction. We will assess our standard NSF paid item fee of $15.00 if the overdraft is a result of a transaction greater than $3.00 but less than $15.01 or a $38.00 NSF paid item fee if the overdraft is a result of a transaction of $15.01 or greater, and the transaction overdraws your account by more than $15.01 (meaning you have a negative $15.00 available balance or more).

If you use our Overdraft Privilege product and we cover a transaction for which there is not enough money in your account to pay, we will consider that an overdraft. We treat all other transactions for which there is not enough money in your account as an NSF transaction, regardless of whether we cover the transaction or the transaction is rejected.

Determining your available balance - With some exceptions, we use the current balance method to determine whether to assess an NSF paid item fee, that is, whether there is enough money in your account to pay for a transaction. For recurring debit-card transactions, certain pre-authorized ACH transactions, everyday debit-card transactions and ATM transactions, we will also not assess an NSF paid item fee if your available balance was sufficient at the time we authorized the transaction even if your current balance is insufficient at the time we pay it during our nightly batch processing. In other words, for those specific transactions above, if your available balance is sufficient when we authorize the transaction or your current balance is sufficient when we pay it, you will not be assessed an NSF paid item fee. Importantly, your “available” balance may not be the same as your account’s “current” balance. Available balance can include memo posts throughout the day. This means an overdraft or an NSF transaction could occur regardless of your account’s available balance.

Your account’s current balance (sometimes called the ledger or actual balance) only includes transactions that have settled up to that point in time, that is, transactions (deposits and payments) that have posted to your account. The current balance does not include outstanding transactions (such as checks that have not yet cleared and electronic transactions that have been authorized but which are still pending). The balance on your periodic statement is the current balance for your account as of the statement date. Your current balance is not updated throughout the day.

The available balance takes transactions, both debits and credits, that have been authorized, but not yet settled, and subtracts or adds them against the current balance. In addition, when calculating your available balance, any “holds” placed on deposits that have not yet cleared are also subtracted from the current balance. For more information on how holds placed on funds in your account can impact your available balance, read the subsection titled “A temporary debit authorization hold affects your account balance.” Your available balance is updated throughout the day. We use your available balance to decide whether to authorize certain transactions (e.g., debit card transactions and ATM withdrawals).

Alpine Bank offers other products and services to help meet your financial needs. Review each product or service terms and conditions independently, as definitions, such as available balance, may differ between them.

Overdrafts - You understand that we may, at our discretion, honor withdrawal requests that overdraw your account. However, the fact that we may honor withdrawal requests that overdraw the account balance does not obligate us to do so later. So you can NOT rely on us to pay overdrafts on your account regardless of how frequently or under what circumstances we have paid overdrafts on your account in the past. We can change our practice of paying, or not paying, discretionary overdrafts on your account without notice to you. You can ask us if we have other account services that might be available to you where we commit to paying overdrafts under certain circumstances, such as an overdraft protection line-of-credit or a plan to sweep funds from another account you have with us. You agree that we may charge fees for overdrafts. For consumer accounts, we will not charge fees for overdrafts caused by ATM withdrawals or one-time (sometimes referred to as “everyday”) debit card transactions if you have not opted-in to that service. (A one-time debit card transaction is a transaction where you use a debit card at a point-of-sale, in an on-line transaction, or in a telephone transaction. The transaction has to be made with a debit card issued by or on behalf of the account-holding institution.) We rely exclusively on how the merchant codes the transaction to determine whether it is “one-time” or “recurring”. We may use subsequent deposits, including direct deposits of social security or other government benefits, to cover such overdrafts and overdraft fees. We will not charge fees for overdrafts caused by transaction $3.00 and below, or transactions that cause less than $15.01 overdraft in the account holder’s account.

Nonsufficient funds (NSF) transactions - If an item drafted by you (such as a check) or a transaction you set up (such as a preauthorized transfer) is presented for payment in an amount that is more than the amount of money in your account, and we decide not to pay the item or transaction, you agree that the item can be returned. Be aware that such an item or payment may be presented multiple times by the merchant or other payee until it is paid, and that we do not monitor or control the number of times a transaction is presented for payment.

Payment types - Some, but not necessarily all, of the ways you can access the funds in your account include debit card transactions, Automated Clearing House (ACH) transactions, and check transactions. All these payment types can use different processing systems and some may take more or less time to post. This information is important for a number of reasons. For example, keeping track of the checks you write and the timing of the preauthorized payments you set up will help you to know what other transactions might still post against your account. For information about how and when we process these different payment types, see the "Payment order of items" subsection below.

Balance information - Keeping track of your balance is important. You can review your balance in a number of ways including reviewing your periodic statement, reviewing your balance online, accessing your account information by phone, or coming into one of our branches.

Funds availability - Knowing when funds you deposit will be made available for withdrawal is another important concept that can help you avoid being assessed fees or charges. Please see our funds availability disclosure (generally titled, “Your Ability to Withdraw Funds”) for information on when different types of deposits will be made available for withdrawal. For an account to which our funds availability policy disclosure does not apply, you can ask us when you make a deposit when those funds will be available for withdrawal. An item may be returned after the funds from the deposit of that item are made available for withdrawal. In that case, we will reverse the credit of the item. We may determine the amount of available funds in your account for the purpose of deciding whether to return an item for non-sufficient funds at any time between the times we receive the item and when we return the item or send a notice in lieu of return. We need only make one determination, but if we choose to make a subsequent determination, the account balance at the subsequent time will determine whether there are insufficient available funds.

A temporary debit authorization hold affects your available balance - On debit card purchases, merchants may request authorization for a specified sum of money when the merchant does not know the exact amount of the purchase at the time the card is authorized. The amount of the authorization request may be more than the actual amount of your purchase. Some common transactions where this occurs involve purchases of gasoline, hotel rooms, or meals at restaurants. When this happens, our processing system cannot determine that the amount of the authorization request exceeds the actual amount of your purchase. This authorization request, and its impact on your available balance account, will eventually be adjusted to the actual amount of your purchase, but it could be three calendar days, or even longer in some cases, before the adjustment is made. Until the adjustment is made, the amount of funds in your account available for other transactions will be reduced by the amount of the temporary hold. If one or more transactions are presented for payment in an amount greater than the funds left after the deduction of the temporary hold amount, you will be charged an NSF or overdraft fee according to our NSF or overdraft fee policy, which may result in one or more overdraft or NSF fees. You will be charged the fee even if you would have had sufficient funds in your account if the amount of the hold had been equal to the amount of your purchase.

Transactions with your debit card - When we authorize a debit card transaction based on your available balance, we may immediately reduce the available balance in your account by the authorization amount requested by the merchant and hold that amount until that transaction is presented by the merchant for payment, or no more than three (3) business days after the date of authorization, whichever first occurs. The final transaction amount presented by the merchant for payment may differ from the amount the merchant originally requested for authorization. If your available balance is insufficient to cover the transaction at the time we authorized it and your current balance is insufficient at the time we pay it, you may be assessed an NSF paid item fee.

Payment order of items - The order in which items are paid is important if there is not enough money in your account to pay all of the items that are presented. The payment order can affect the number of items overdrawn or returned unpaid and the amount of the fees you may have to pay. To assist you in managing your account, we are providing you with the following information regarding how we process those items.

Payment order on DDA & Savings accounts - Credits/deposits (items being added to your balance) are always posted first in the account. Debits (item being deducted from your balance) generally will post in the following order: The list provided does not include all possible debit items, but rather a broad overview of common transactions. Alpine Bank will clear each item within these stated categories before proceeding to the next category.

- Common Fees - For example, a non-Alpine/non-Allpoint ATM fee, a Chargeback item fee, or an account service fee;

- Transfers between your Alpine bank accounts;

- Telephone Transfers - Transfers you have initiated by telephone between your Alpine accounts;

- ATM withdrawals;

- Automated Clearing House (ACH) - Electronic payments that are made directly from your Alpine account to: other financial institutions; payment services,such as PayPal and; other businesses;

- Point of Sale (POS) or One-time Debit Card Transactions – Everyday transactions usually made with a merchant using a debit card;

- Checks - Generally post based on sequential check number order received, lowest to highest; and

- NSF Paid Item fees - Collect and post last.

If you have two items within the same categories as indicated above generally those items will post based on serial number (low to high); if those items within the stated category lack a serial number, the items will then post in a predetermined numeric order by category, if more than one item falls in the same category then it will post smallest dollar amount to the largest dollar amount.

If a check, item or transaction is presented for payment without a sufficient current balance in your account to pay it, we may, at our discretion, pay the item (creating an overdraft fee) or return the item for non-sufficient funds (NSF). An authorized debit card transaction will be paid upon presentment for payment regardless of the current balance at the time of presentment. The amounts of the overdraft fees, if we pay the item, are disclosed in the Fee Schedule, and your rights to opt-in to overdraft services. We will not charge you an NSF returned item fee for items that are returned unpaid. We encourage you to make careful records and practice good account management. This will help you to avoid creating items without sufficient funds and potentially incurring the resulting fees.

BUSINESS, ORGANIZATION AND ASSOCIATION ACCOUNTS - Earnings in the form of interest, dividends, or credits will be paid only on collected funds, unless otherwise provided by law or our policy. You represent that you have the authority to open and conduct business on this account on behalf of the entity. We may require the governing body of the entity opening the account to give us a separate authorization telling us who is authorized to act on its behalf. We will honor the authorization until we actually receive written notice of a change from the governing body of the entity.

STOP PAYMENTS - The rules in this section cover stopping payment of common items such as checks and drafts, followed by specific rules for electronic fund transfers (e.g., Automated Clearing House). If you have questions about rules we have not disclosed to you here or elsewhere, you may ask us about those rules. We may assess a Stop Payment Fee for each stop payment request. Please refer to the "Fee Schedule".

We may accept an order to stop payment on any item from any one of you. You must make any stop-payment order in the manner required by law and we must receive it in time to give us a reasonable opportunity to act on it before our stop-payment cutoff time. Because the most effective way for us to execute a stop-payment order is by using an automated process, to be effective, your stop-payment order must precisely identify the number, date, and amount of the item, and the payee. You may stop payment on any item drawn on your account whether you sign the item or not. Generally, if your stop-payment order is given to us orally or in writing it is effective for six months. Your order will lapse after that time if you do not renew the order in writing before the end of the six-month period. If the original stop-payment order was oral your stop-payment order may lapse after 14 calendar days if you do not confirm your order in writing within that time period. We are not obligated to notify you when a stop-payment order expires. In all instances, if a stop payment order is $10,000.00 or more, Alpine Bank will require a written authorization that includes a signature. A release of the stop-payment request may be made by any person who has ownership of the account the item was presented against.

If you stop payment on an item and we incur any damages or expenses because of the stop payment, you agree to indemnify us for those damages or expenses, including attorneys' fees. You assign to us all rights against the payee or any other holder of the item. You agree to cooperate with us in any legal actions that we may take against such persons. You should be aware that anyone holding the item may be entitled to enforce payment against you despite the stop-payment order.

Our stop-payment cutoff time is one hour after the opening of the next banking day after the banking day on which we receive the item. Additional limitations on our obligation to stop payment are provided by law (e.g., we paid the item in cash or we certified the item).

ACH STOP PAYMENTS - Excluding the following requirements as defined in this section, all provisions stated above are also applicable to stop payments for Automatic Clearing House items. Generally, if your stop-payment order is given to us in writing it is effective for six months. Your order will lapse after that time if you do not renew the order in writing before the end of the six-month period. If the original stop-payment order was oral your stop-payment order will lapse after 14 calendar days if you do not confirm your order in writing within that time period. We are not obligated to notify you when a stop-payment order expires. A release of the stop-payment request may be made by any person who has ownership of the account the item was presented against. To remain in effect for more than 14 calendar days, all stop-payment orders for an electronic fund transfer, regardless of the dollar amount, will require a written authorization that includes a signature.

Our stop-payment cutoff time for ACH items is no less than three business days before an item has been received by Alpine Bank, otherwise Alpine Bank cannot guarantee the effectiveness of the stop-payment order. Additional limitations on our obligation to stop payment are provided by law.

TELEPHONE TRANSFERS - A telephone transfer of funds from this account to another account with us, if otherwise arranged for or permitted, may be made by the same persons and under the same conditions generally applicable to withdrawals made in writing. Limitations on the number of telephonic transfers from a savings account, if any are described elsewhere.

AMENDMENTS AND TERMINATION - We may amend, alter, change, or add new terms to this Agreement by sending you a notice or including a message on or with your account statement. The notice or statement will be sent to the address shown on our deposit records, or, if applicable, you will be notified of its availability electronically. We may change our fee schedules subject to any notice required by law. Although your acceptance of a change may not be required, your continued use of your account after the effective date of any amendment, alteration, change or added new terms to, or after a reasonable time, not to exceed ten (10) calendar days, if no such date is stated, will constitute your acceptance of the terms of the amendment, alteration, change or added new terms. We may amend, alter, change, add new terms to the fee schedules or other terms applicable to a particular account, based upon the account relationship and other factors. For any of these types of changes, we will give you reasonable notice in writing by any reasonable method including by mail, by any electronic communication method to which you have agreed, on or with a periodic statement, or through any other method permitted by law.

Unless otherwise indicated in the notice of change, if we have notified you of a change to your account, and you continue to have your account after the effective date of the change, you have accepted and agreed to the new or modified terms. You should review any change in terms notice carefully as the notice will provide important information of which you may need to be aware. We reserve the right to waive any term of this agreement. However, such waiver shall not affect our right to enforce the term at a later date.

Closing the Account - You or the Bank may close your account at any time, for any reason, upon reasonable notice. Reasonable notice depends on the circumstances, and in some cases, such as when we cannot verify your identity or we suspect fraud, it might be reasonable for us to give you notice after the change becomes effective. For instance, if we suspect fraudulent activity with respect to your account, and if we deem it appropriate under the circumstances and necessary to prevent further fraud, we might immediately freeze or close your account and then give you notice.

If you request that we close your account, we may ask that you provide your request in writing. You are responsible for leaving enough money in the account to cover any outstanding items or transactions to be paid from the account. We are not required to close the Account at your request until all known authorized or outstanding items (including, but not limited to, checks, ATM, point-of-sale, ACH and other electronic transactions) have been paid from your Account and any outstanding disputes (including but not limited to disputes regarding electronic transfers, ACH transactions or other unresolved internal research requests/disputes concerning the Account) have been resolved. After you or we close the Account the tender of the account balance, if any, will be provided to you or your agent personally, by mail or by another agreed upon method. The tender of the account balance will be reduced by any amount you owe us. You will still be responsible for any outstanding transactions, service charges or fees or overdrafts incurred before, during or after the time the Account is closed.

After your Account is closed, we may temporarily reopen your Account to resolve a dispute concerning the Account, or to accept a debit or credit to your Account, even if doing so results in your Account becoming overdrawn. If we temporarily reopen your Account, we may exercise our discretion to return any debit or credit that is received to your Account while your Account is temporarily reopened. If we receive a debit or credit to your Account after it is closed, we may, in our sole discretion, return to the payee any debit or return to the originator any additional deposits or electronic credits (including, but not limited to, Social Security, pension payments and automatic payroll deposits), and you will be liable for any associated charges or fees. We may close your account due to an outstanding negative balance. If your account remains consecutively overdrawn for 59 calendar days, we will begin the account closure process. If the 59th calendar day falls on a weekend or a federally recognized holiday, your account will be closed the business day before the weekend or holiday. If we close your account, any amounts owed may be pursued through applicable legal collection actions. In addition, we may report the unsatisfactory status of your account to the credit bureaus or other consumer reporting agencies. Late payments, missed payments, or other defaults on your account may be reflected in your credit report or other consumer reports. We will also consider that you have closed your account if the balance of the account is $0.00 for 60 consecutive calendar days. If your account balance remains $0.00 for 60 calendar days, we will close the account on the 61st business day. Business Day is defined as any day in which Alpine Bank is open to the public for carrying on substantially all of its business functions. This generally includes Monday through Friday, excluding weekends and federal holidays as specified in 5 U.S.C.A. §6103(a). Any items and transactions presented for payment after the account is closed may be dishonored. Any deposits we receive after the account is closed may be returned. We will not be liable for any damages for not honoring any such debits or deposits received after the account is closed.

Note: Rules governing changes in interest rates are provided separately in the Truth-in-Savings disclosure or in another document. In addition, for changes governed by a specific law or regulation, we will follow the specific timing and format notice requirements of those laws or regulations.

CORRECTION OF CLERICAL ERRORS - Unless otherwise prohibited by law, you agree, if determined necessary in our reasonable discretion, to allow us to correct clerical errors, such as obtaining your missing signature, on any account documents or disclosures that are part of our agreement with you. For errors on your periodic statement, please refer to the STATEMENTS section.

NOTICES - Any written notice you give us is effective when we actually receive it, and it must be given to us according to the specific delivery instructions provided elsewhere, if any. We must receive any notice in time to have a reasonable opportunity to act on it. If a notice is regarding a check or other item, you must give us sufficient information to be able to identify the check or item, including the precise check or item number, amount, date and payee. Notice we give you via the United States Mail is effective when it is deposited in the United States mail with proper postage and addressed to your mailing address we currently have on file. Notice we give you through your email of record, or other electronic method to which you agreed, will be treated as delivered to you when sent. Notice to any of you is notice to all of you.

STATEMENTS - Your duty to report unauthorized signatures (including forgeries and counterfeit checks) and alterations on checks and other items - You must examine your statement of account with "reasonable promptness." If you discover (or reasonably should have discovered) any unauthorized signatures, including forgeries and counterfeit checks or alterations, or any other indication of forgery or counterfeiting, you must promptly notify us of the relevant facts. As between you and us, if you fail to do either of these duties, you will have to either share the loss with us, or bear the loss entirely yourself (depending on whether we used ordinary care and, if not, whether we contributed to the loss). The loss could be not only with respect to items on the statement but other items with unauthorized signatures or alterations by the same wrongdoer.

You agree that the time you have to examine your statement and report to us will depend on the circumstances, but will not, in any circumstance, exceed a total of 30 days from when the statement is first sent or made available to you.

You further agree that if you fail to report any unauthorized signatures or alterations in your account within 30 days of when we first send or make the statement available, you cannot assert a claim against us on any items in that statement, and as between you and us the loss will be entirely yours. This 30-day limitation is without regard to whether we used ordinary care. The limitation in this paragraph is in addition to that contained in the first paragraph of this section.

Your duty to report other errors or problems - In addition to your duty to review your statements for unauthorized signatures, and alterations you agree to examine your statement with reasonable promptness for any other error or problem - such as an encoding error or an unexpected deposit amount. Also, if you receive or we make available either your items or images of your items, you must examine them for any unauthorized or missing indorsements or any other problems. You agree that the time you have to examine your statement and items and report to us will depend on the circumstances. However, this time period shall not exceed 30 days. Failure to examine your statement and items and report any errors to us within 30 days of when we first send or make the statement available precludes you from asserting a claim against us for any errors on items identified in that statement and as between you and us the loss will be entirely yours.

Duty to notify if statement not received - You agree to immediately notify us if you do not receive your statement by the date you normally expect to receive it. Not receiving your statement in a timely manner is a sign that there may be an issue with your account, such as possible fraud or identity theft. Absent a lack of ordinary care by us, a failure to receive your statement in a timely manner does not extend the time you have to conduct your review under this agreement.

ACCOUNT TRANSFER - This account may not be transferred or assigned without our prior written consent.

REIMBURSEMENT OF FEDERAL BENEFIT PAYMENTS - If we are required for any reason to reimburse the federal government for all or any portion of a benefit payment that was directly deposited into your account, you authorize us to deduct the amount of our liability to the federal government from the account or from any other account you have with us, without prior notice and at any time, except as prohibited by law. We may also use any other available legal remedy to recover the amount of our liability.

TEMPORARY ACCOUNT AGREEMENT - If the account documentation indicates that this is a temporary account agreement, it means that all account owners have not yet signed the signature card, or that some other account opening requirement has not been met. Each person who signs to open the account or has authority to make withdrawals (except as indicated to the contrary) may transact business on this account. However, we may at some time in the future restrict or prohibit further use of this account if you fail to comply with the requirements we have imposed within a reasonable time.

SETOFF - We may (without prior notice and when permitted by law) set off the funds in this account against any due and payable debt any of you owe us now or in the future. If your debt arises from a promissory note, then the amount of the due and payable debt will be the full amount we have demanded, as entitled under the terms of the note, and this amount may include any portion of the balance for which we have properly accelerated the due date.

This right of setoff does not apply to this account if prohibited by law. For example, the right of setoff does not apply to this account if: (a) it is an Individual Retirement Account or similar tax-deferred account, or (b) the debt is created by a consumer credit transaction under a credit card plan (but this does not affect our rights under any consensual security interest), or (c) the debtor's right of withdrawal only arises in a representative capacity. We will not be liable for the dishonor of any check when the dishonor occurs because we set off a debt against this account. You agree to hold us harmless from any claim arising as a result of our exercise of our right of setoff.

RESTRICTIVE LEGENDS OR INDORSEMENTS - The automated processing of the large volume of checks we receive prevents us from inspecting or looking for restrictive legends, restrictive indorsements or other special instructions on every check. For this reason, we are not required to honor any restrictive legend or indorsement or other special instruction placed on checks you write unless we have agreed in writing to the restriction or instruction. Unless we have agreed in writing, we are not responsible for any losses, claims, damages, or expenses that result from your placement of these restrictions or instructions on your checks. Examples of restrictive legends placed on checks are "must be presented within 90 days" or "not valid for more than $1,000.00." The payee's signature accompanied by the words "for deposit only" is an example of a restrictive indorsement.

FACSIMILE/ELECTRONIC SIGNATURES - You authorize us at any time, to charge you for all checks, drafts or other orders for the payment of money (instruments) utilizing a facsimile or electronic signature(s), which are drawn on us regardless of by whom or by what means the facsimile/electronic signature(s) may have been affixed. This authorization specifically includes forged or counterfeit instruments using a facsimile/electronic signature, and you agree to be solely responsible for any loss which may be incurred by virtue of the use of facsimile/electronic signature(s) under this paragraph. You expressly assume all risks involved with any unauthorized use of such facsimile/electronic signature(s) and agree that you shall be responsible for and chargeable with the amount of all instruments bearing such facsimile/electronic signature(s) or signatures resembling the same, whether or not authorized by you. This agreement is made pursuant to C.R.S. §4-4-103(a) and is intended to allow variation of the normal allocation of losses from forged checks based on the provisions of the Uniform Commercial Code.

CHECK PROCESSING - We process items mechanically by relying almost exclusively on the information encoded in magnetic ink along the bottom of the items. This means that we do not individually examine all of your items to determine if the item is properly completed, signed and indorsed or to determine if it contains any information other than what is encoded in magnetic ink. You agree that we have exercised ordinary care if our automated processing is consistent with general banking practice, even though we do not inspect each item. Because we do not inspect each item, if you write a check to multiple payees, we can properly pay the check regardless of the number of indorsements unless you notify us in writing that the check requires multiple indorsements. We must receive the notice in time for us to have a reasonable opportunity to act on it, and you must tell us the precise date of the check, amount, check number and payee. We are not responsible for any unauthorized signature or alteration that would not be identified by a reasonable inspection of the item. Using an automated process helps us keep costs down for you and all account holders.

AUTOMATED PROCESSING OF ITEMS - Because of the automated nature of processing a high volume of items, most checks and other items are processed automatically, i.e., without our individual review of each item. While we examine items pursuant to a random sampling of items drawn on all accounts or a procedure that meets certain minimum criteria that we may establish for inspection, you agree that we are exercising ordinary care and common and reasonable banking practices by automatically processing checks, and other items.

CHECK CASHING - We may charge a fee for anyone that does not have an account with us who is cashing a check, draft or other instrument written on your account. We may also require reasonable identification to cash a check, draft or other instrument. We can decide what identification is reasonable under the circumstances and such identification may be documentary or physical and may include collecting a thumbprint or fingerprint.

INDORSEMENTS - We may accept for deposit any item payable to you or your order, even if they are not indorsed by you. We may give cash back to any one of you. We may supply any missing indorsement(s) for any item we accept for deposit or collection, and you warrant that all indorsements are genuine.

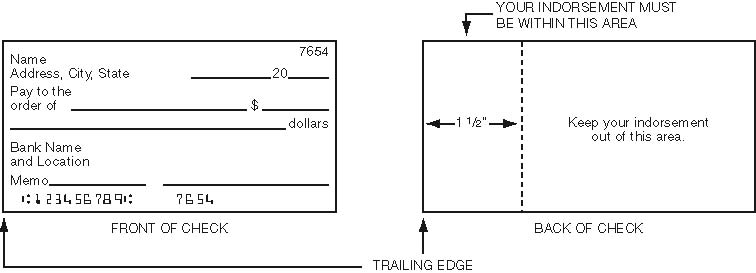

To ensure that your check or share draft is processed without delay, you must indorse it (sign it on the back) in a specific area. Your entire indorsement (whether a signature or a stamp) along with any other indorsement information (e.g. additional indorsements, ID information, driver's license number, etc.) must fall within 11/2" of the "trailing edge" of a check. Indorsements must be made in blue or black ink, so that they are readable by automated check processing equipment.

As you look at the front of a check, the "trailing edge" is the left edge. When you flip the check over, be sure to keep all indorsement information within 11/2" of that edge.